Active Business Income Formula

The IRS says you have an excess loss if your total business deductions are more than your total gross income and your business profits plus 250000 or 500000 for a joint return. Active income is typically anything other than investment income rental income leasing income income from a specified investment business or a personal services business.

How To Pay Little To No Taxes For The Rest Of Your Life

How To Pay Little To No Taxes For The Rest Of Your Life

For purposes of achieving the most favourable Canadian tax rates see Small Business Deduction later in this book this Active Business Income must be generated in.

Active business income formula. The limit is set in subsection 1252. This deduction will apply to the ABI as defined above up to the business limit. Active Business Income.

Note that the 500000 annual business limit must be shared among associated corporations. 18 the lesser of. An assessable dividend is an amount received by a corporation as on account of in lieu of payment of or in satisfaction of a taxable dividend to the extent that amount is deductible from taxable income under section 112.

There is no need to complete schedule 7 if there is no other property income for a corporation. Income earned by a C corporation or by providing services as an employee isnt eligible for the deduction. Rental and leasing income may qualify as active income in certain situations.

It is relevant to the tax integration mechanism and refundable dividends. Active Business Income Income Tax Act s. Dividend distributed to shareholder.

Active income refers to income received from performing a service. Portfolio income including interest other than self-charged interest treated as passive activity income discussed later dividends annuities and royalties not derived in the ordinary course of a trade or business and gain or loss from the disposition of property that produces portfolio income or is held for investment see section 163d. Active business income is essentially exactly what is sounds like.

Your income from an active business carried on in Canada eligible for the small business deduction including any specified corporate income as defined in subsection 1257 Use this schedule if another CCPC is making an assignment of business limit under subsection 12532 to you. Learn if your business qualifies for the QBI deduction of up to 20. This calculates your businesss earnings before tax.

Active Business Income ABI earned in Canada. Business income is any income realized as a result of business activity. Income from most businesses qualifies as active business income.

As previously mentioned all the allowable expenses can be deducted. Per ITA 1257 active business income means any business carried on by the corporation other than a specified investment business or a personal services business. 1257 The first 500000 business limit for 2012 federally of active business income of a Canadian controlled private corporation or CCPC is taxed at lower rates.

Deduct taxes from this amount to find you businesss net income. 500000 annual limit less amount of shared by associated corporations. Such an income is known as Active Business Income ABI.

The deduction allows them to deduct up to 20 percent of their qualified business income QBI plus 20 percent of qualified real estate investment trust REIT dividends and qualified publicly traded partnership PTP income. These types of income are usually passive income and passive income does not qualify for the small business deduction. At incomes below that level the deduction is 20 of either taxable income minus capital gains and dividends or the QBI whichever is less.

Rental income from associated corporations is an active business income if the associated corporation is engaged in an active business. To say it more simply taking any loss more than 250000 single taxpayer 500000 joint return is considered excess and that excess amount cant be taken as a loss on your tax return for the year. General Formula Amount Calculation.

Corporate tax payable 15000 100000 15 Federal Ontario Equals. Canadian Controlled Private Corporations CCPC carrying a business in Canada can deduct from the tax otherwise payable an amount known as a small business deduction. This includes wages tips salaries commissions and income from businesses in which there is material participation.

The tax reduction is called the small business deduction. The Qualified Business Income QBI Deduction is a tax deduction for pass-through entities. Calculate your total revenue.

IT-73R6 The Small Business. Subtract your businesss expenses and operating costs from your total revenue. Once the taxable income reaches or exceeds 163300 326600 if filing jointly the type of business also comes into play.

Dividend gross-up 17 non-eligible dividend rate 14450. Business income is a type of earned income and is classified as ordinary income for tax purposes.

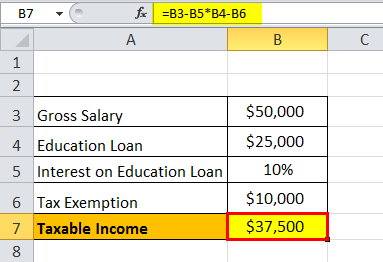

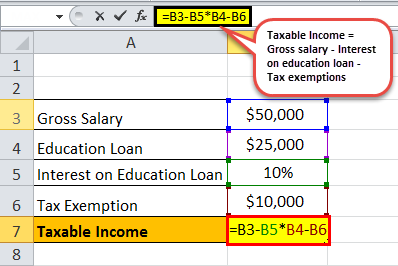

Taxable Income Formula Examples How To Calculate Taxable Income

Taxable Income Formula Examples How To Calculate Taxable Income

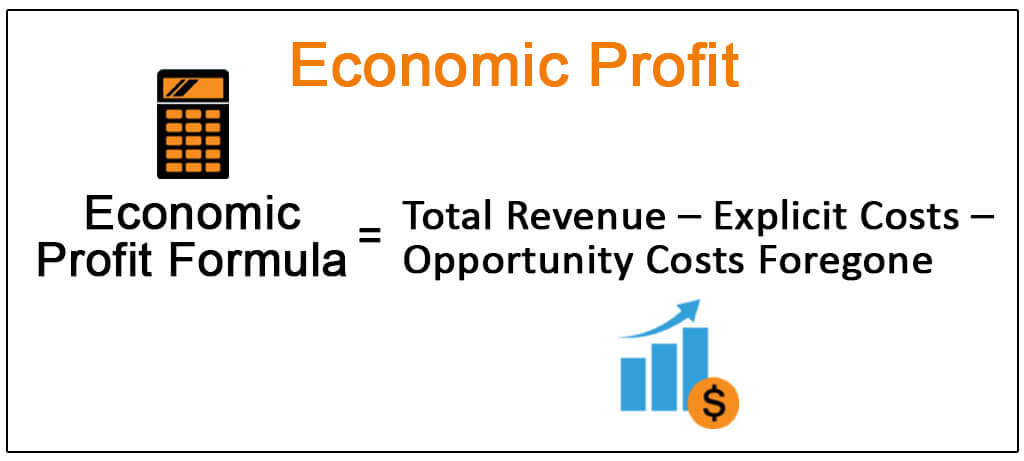

Economic Profit Definition Interpretation Limitations

Economic Profit Definition Interpretation Limitations

Corporate Profit Definition Example How To Calculate

Corporate Profit Definition Example How To Calculate

Gross Income Module 2 Computing The Tax Coursera

Gross Income Module 2 Computing The Tax Coursera

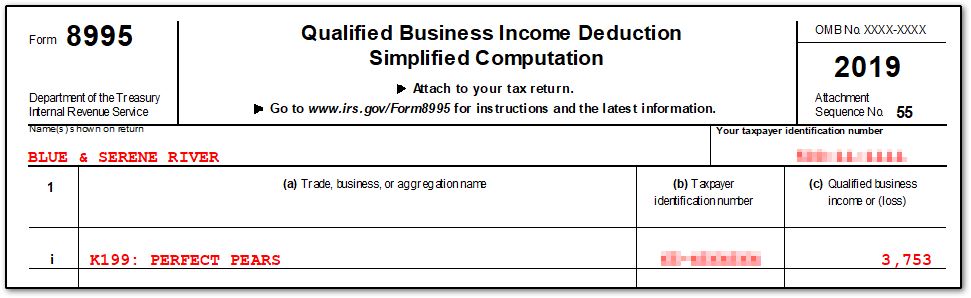

Form 8995 A Schedule C Loss Netting And Carryforward K1 Schedulec Schedulee Schedulef

Form 8995 A Schedule C Loss Netting And Carryforward K1 Schedulec Schedulee Schedulef

Qbi Deduction Frequently Asked Questions Qbi Schedulec Schedulee Schedulef W2

Qbi Deduction Frequently Asked Questions Qbi Schedulec Schedulee Schedulef W2

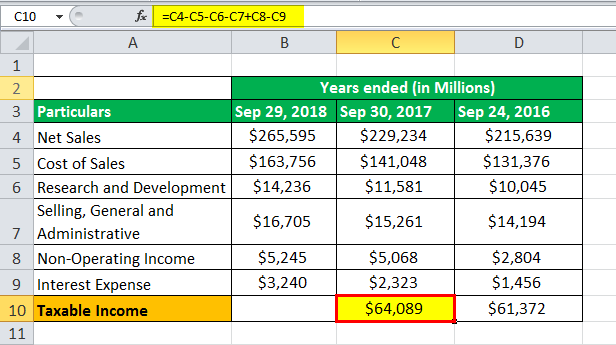

How To Calculate Corporate Taxable Income In Canada Mileiq Canada

How To Calculate Corporate Taxable Income In Canada Mileiq Canada

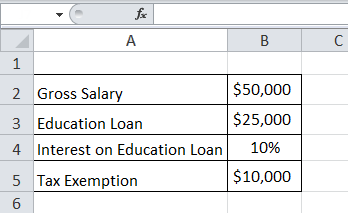

Taxable Income Formula Examples How To Calculate Taxable Income

Taxable Income Formula Examples How To Calculate Taxable Income

Taxable Income Formula Examples How To Calculate Taxable Income

Taxable Income Formula Examples How To Calculate Taxable Income

Qbi Deduction Frequently Asked Questions Qbi Schedulec Schedulee Schedulef W2

Qbi Deduction Frequently Asked Questions Qbi Schedulec Schedulee Schedulef W2

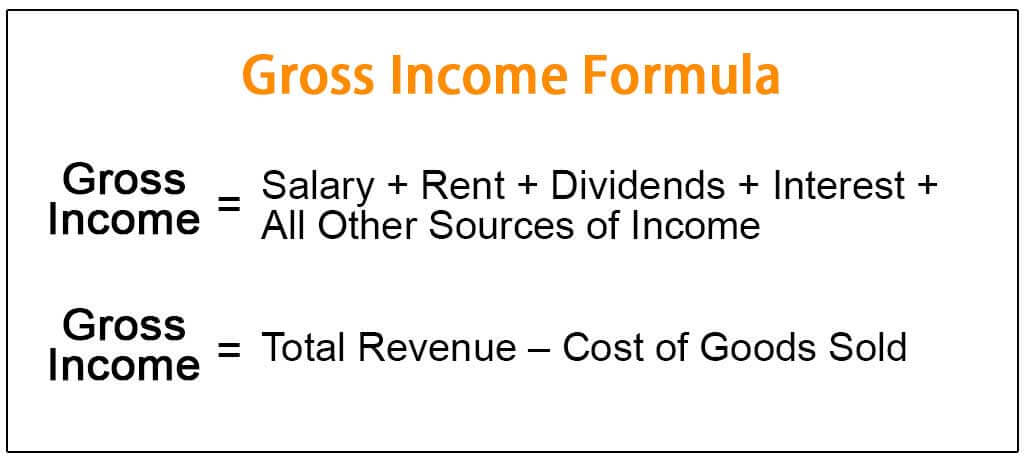

Gross Income Formula Step By Step Calculations

Gross Income Formula Step By Step Calculations

Form 8995 A Schedule C Loss Netting And Carryforward K1 Schedulec Schedulee Schedulef

Form 8995 A Schedule C Loss Netting And Carryforward K1 Schedulec Schedulee Schedulef

Corporate Tax Meaning Formula Examples Calculations

Corporate Tax Meaning Formula Examples Calculations

How To Pay Little To No Taxes For The Rest Of Your Life

Profit Before Tax Formula Examples How To Calculate Pbt

Profit Before Tax Formula Examples How To Calculate Pbt

Corporate Tax Meaning Formula Examples Calculations

Corporate Tax Meaning Formula Examples Calculations

Taxable Income Formula Examples How To Calculate Taxable Income

Taxable Income Formula Examples How To Calculate Taxable Income

Corporate Tax Meaning Formula Examples Calculations

Corporate Tax Meaning Formula Examples Calculations

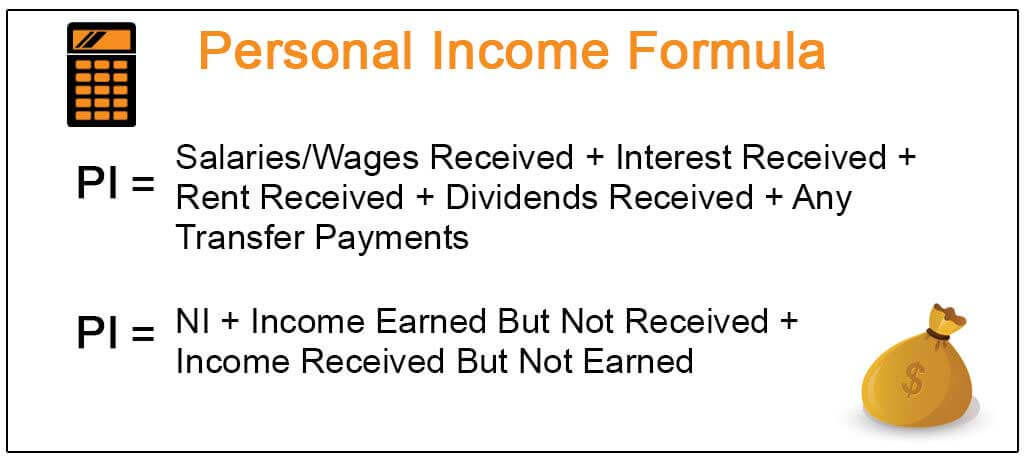

Personal Income Definition Formula How To Calculate

Personal Income Definition Formula How To Calculate